/

•

•

Detailed stories on technology startups, business and economic current affairs.

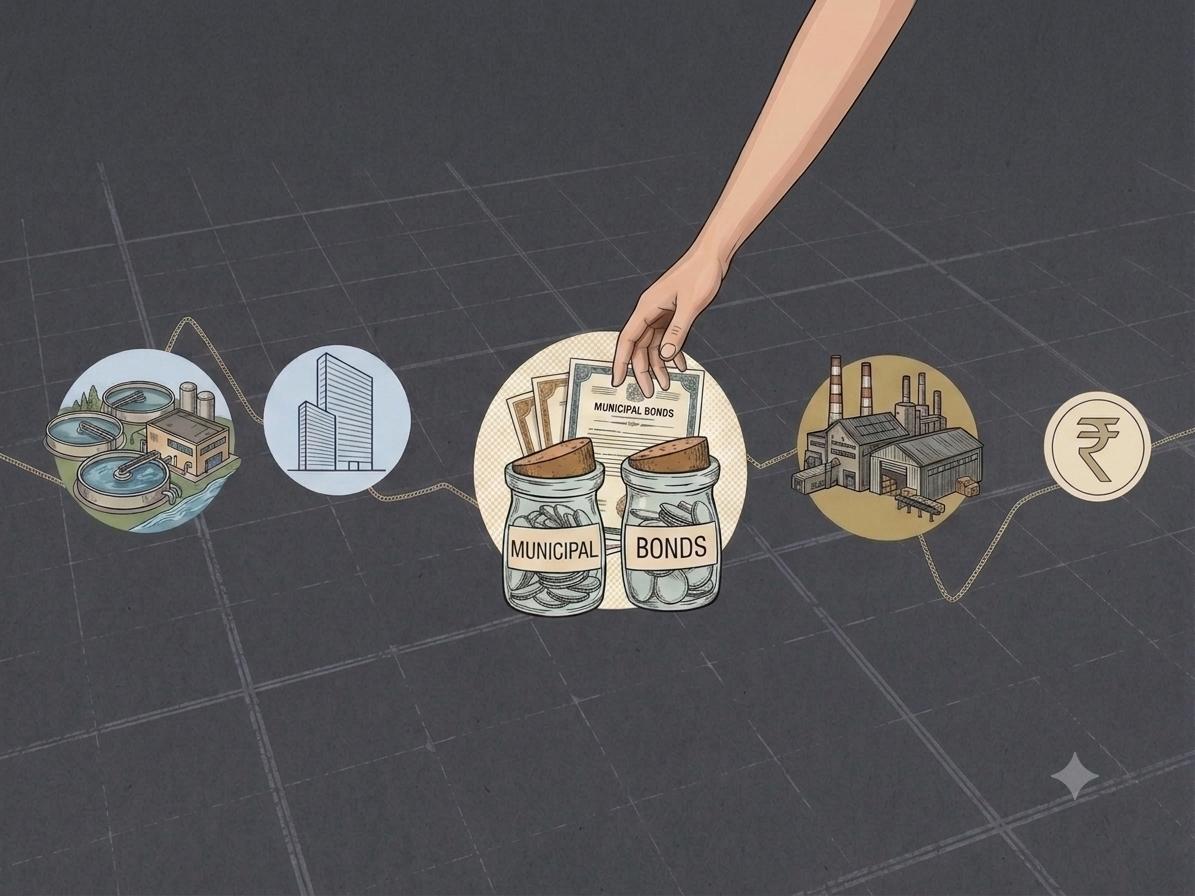

The budget’s big infrastructure push, along with rising FDI inflows, is expected to fire up the economy.

Editor's note: Finance minister Nirmala Sitharaman, in her budget speech on Monday, proposed that the government spend Rs 5.54 lakh crore on infrastructure projects next fiscal. That's a whopping 35% jump from the previous year’s figure. This, she said, would help revive the $2.8 trillion economy and spur growth. The plan is audacious because in the year gone by, the Indian economy contracted for the first time in four decades, thanks to the COVID-19 pandemic. The government's revenues saw a steep drop as a series of lockdowns to tackle its spread brought industry and business to a grinding halt. Further, it had to spend way more that was budgeted on welfare schemes, leaving it with a gaping fiscal deficit. But there was no hint of all that in Sitharaman’s speech. She made clear her intention to spend her way out of trouble by building roads, metro rail networks and bridges to reinvigorate the economy. What makes the proposed infrastructure capex stand out is that the budget refrained from putting any additional burden on taxpayers. In fact, it is now being touted as …

Fiscal discipline holds on paper, but the number is propped up by higher borrowing and revenue sources that are far from stable.

Whatever be the outcome, the India-US trade deal's impact on economic growth and sovereignty cannot be separated.

Your tax money should go into making your life better. It would appear it is instead funding the lifestyle of venture capitalists and founders of uncertain, loss-making businesses.